Bitcoin Academy: Part 3

Bitcoin as a Protocol: Paired Keys & Proof-of-Work Mining

The Bitcoin protocol is essentially the rulebook that every node follows to maintain and update the ledger. It’s like the constitution of the Bitcoin network, defining how transactions work, how the ledger is structured, and how participants come to agreement (consensus) on the history of transactions. Two of the most important aspects of the protocol are: (a) how Bitcoin uses cryptography to define and secure ownership of funds, and (b) how Bitcoin achieves decentralized consensus on new transactions (preventing cheating like double-spending). Let’s break each of those down.

Ownership via Cryptography: Private Keys and Addresses

So, if there are no physical coins or centralized accounts, what does it mean to “own” Bitcoin? In Bitcoin, ownership is purely cryptographic. Possession of a Bitcoin simply means you control a secret digital key that grants you the right to move an entry in the ledger. This leverages the principles of public-key cryptography that we encountered in Part 1 (recall that in 1976, Whitfield Diffie and Martin Hellman introduced the idea of having paired keys: one public, one private). Every Bitcoin “account” or address is derived from a public key, and has a corresponding private key known only by the owner. We can summarize it as follows:

Public Key (Public Address): This is like your account number or a deposit address. It’s a string of letters and numbers that anyone can use to send you bitcoin. You can share it freely—it does not give anyone control, it only tells the network “if someone sends bitcoin to this address, update the ledger to credit that address.”* Think of it like a locked mailbox on the street: anyone can drop money in by knowing your address.

* Private Key: This is like the key to that mailbox—a secret passcode that allows you to access and spend the bitcoin associated with your address. When you want to send Bitcoin to someone else, your wallet software creates a transaction and digitally signs it with your private key. This digital signature is mathematically linked to your public key and proves that the owner of that address authorized the transaction. The beauty is that nodes can verify the signature using the public key without ever seeing your private key, thanks to cryptography. If the signature is valid, the network knows that the transaction is legitimate and the person sending the funds truly has the right to spend them.

This concept of self-custody (that you control your own money via cryptographic keys) is revolutionary. It empowers individuals to be their own “bank,” addressing the Part 1 issue of having to trust institutions to hold and manage your funds. You are not relying on a bank’s promise or a government’s backing; you either have the key to spend your coins, or you don’t. There’s no in-between and no third party who can override that. This freedom, of course, comes with great responsibility. If you lose your private key, there is no password-reset or customer support to call. The coins associated with that key are effectively lost forever because nobody else (not even the network) can generate the same signature. In Bitcoin, a common saying is “not your keys, not your coins.” If you entrust your private keys to someone else (like an exchange or custodial wallet), you’re back in a situation of having to trust a third party. Bitcoin gives you the option to eliminate that trust by holding your own keys, putting control and risk squarely in your hands. In Bitcoin, code and cryptography replace the need to trust human institutions—the rules are enforced by unbreakable math rather than fallible middlemen.

Proof-of-Work, explained

Now we know what the Bitcoin ledger is (a shared record) and how ownership is controlled (by public/private keys and digital signatures). But there’s another critical puzzle: How do all those independent nodes agree on updates to the ledger? In other words, when new transactions like “Alice pays 1 bitcoin to Bob” are broadcast, who gets to add them to the official ledger, and in what order? And how do we prevent someone from cheating, say by trying to spend the same bitcoin twice in two different places (the infamous double-spending problem)? Without a central authority, this was a very hard problem to solve. This is the problem Satoshi Nakamoto’s whitepaper famously tackled.

The Proof-of-Work Mining Process

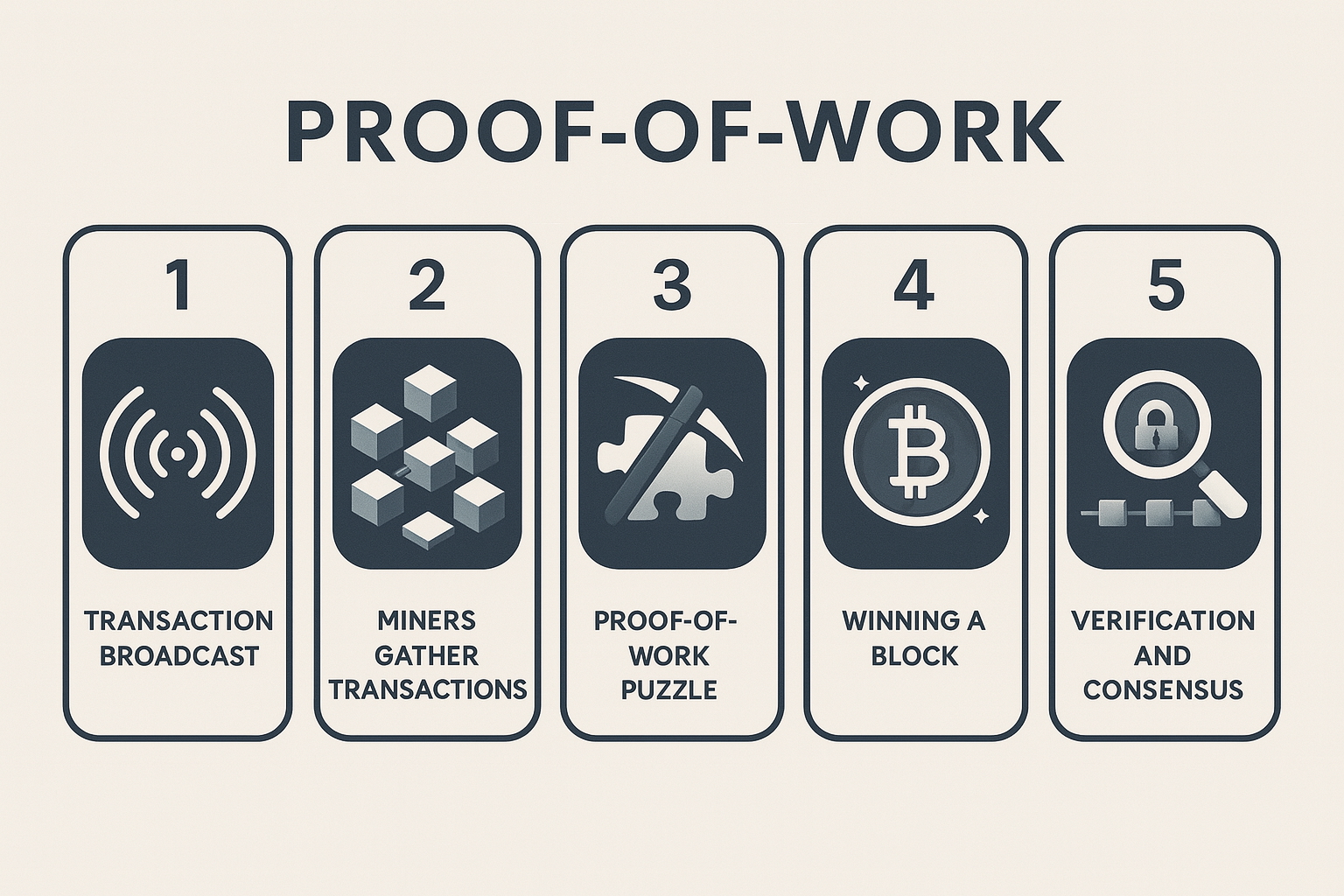

Bitcoin’s breakthrough is a system called Proof-of-Work mining, which allows the network of nodes to reach consensus on the history of transactions without any central trusted party. It works like a decentralized competition or lottery among the nodes:

1. Transaction Broadcast: When Alice sends Bitcoin to Bob, that transaction is sent out to the network. Every node that receives it will check that it’s valid (correct signature, Alice has enough balance, etc.), then relay it to others. So transactions spread peer-to-peer. Valid transactions enter a pool of pending transactions waiting to be added to the ledger.

2. Miners Gather Transactions into a Block: Some special nodes called miners take pending transactions and package them into a block, like assembling a new page of the ledger. Each block also links to the previous block (forming a chain, hence “blockchain”).

3. Proof-of-Work Puzzle: To qualify to add their block, a miner must solve a tough mathematical puzzle that the network generates. Solving this puzzle requires the miner’s computers to brute-force trillions of guesses—a process that consumes a lot of electricity and processing power. It’s like a lottery or a guess-the-number game: each hash attempt is a “ticket.”

4. Winning a Block: Approximately every 10 minutes, one lucky miner finds a valid solution that the protocol deems acceptable. This miner “wins” the round and earns the right to add their block of transactions to the blockchain. They immediately broadcast this new block to the whole network.

5. Verification and Consensus: Upon receiving the new block, all the other nodes verify it. They check that the Proof-of-Work solution is correct (which is easy to do once it’s found), and that all the transactions in the block are valid (no double-spends, correct signatures, no one creating coins out of thin air, etc.). If the block checks out, the nodes accept it and update their copy of the ledger to include the new transactions. Any pending transactions that were included in that block are now considered settled. With this, a new round begins for the next block, with miners now competing to extend the chain further.

This mining process might sound complex, but the main takeaway is this: Proof-of-Work makes cheating or falsifying the ledger extremely costly and difficult. Why? Because if a bad actor wanted to, say, insert a fake transaction or modify an old one, they wouldn’t just need to do it on one computer. They’d need to re-do all the Proof-of-Work that has been done on that block and every block after it, and outpace the entire rest of the network of honest miners who continue to add new blocks on top. The longest chain of blocks (with the most cumulative work) is considered the valid history. Unless you have more computational power than everyone else combined, you won’t be able to catch up and surpass the legitimate chain. In essence, the system trusts the longest chain—and the longest chain represents the most work done (hence most computational “proof” of legitimacy). Satoshi described this elegantly: “It doesn’t matter who tells you the longest chain, the Proof-of-Work speaks for itself.”. Nodes automatically follow the chain with the most Proof-of-Work behind it, so no coercion or central authority is needed—the energy expended secures the network’s consensus.

Another way to think of it: Bitcoin’s security comes from the fact that cheating requires doing an astronomically impractical amount of work. As long as the majority of miners are honest (following the incentives to earn the block reward by mining within the rules), their combined work will outweigh any attacker’s work, and thus honest consensus will always win out. The game theory is set up so that attacking Bitcoin would be prohibitively expensive and likely futile, whereas following the rules and mining honestly is profitable. It flips the trust model: you don’t have to trust any particular miner or node; you trust the aggregate Proof-of-Work done by the majority.

The Proof-of-Work Mining Reward System

Why would anyone participate in this expensive mining race? The Bitcoin protocol rewards miners for their work. When a miner successfully mines a block, they get to claim a block reward: new bitcoin created by the protocol (plus any transaction fees from the block’s transactions) go to the miner as a prize. This is how new bitcoin enter circulation—through mining rewards. In Bitcoin’s early days, the reward was 50 bitcoin per block; currently it’s 3.125 bitcoin, and it will continue to decrease over time (more on that in the next section). The reward creates a strong incentive for people to devote computing power to mining, which in turn secures the network. As computer scientist and early Bitcoin developer Hal Finney noted, mining is healthiest when it’s just barely profitable—if it’s too easy and profitable, more miners will join until the competition (and difficulty) rises, ensuring that no one miner can easily dominate. “Ultimately it’s good for the network for mining to be expensive. It makes it that much harder for a well-financed attacker to dominate the network,” Finney explained. In other words, the expense and effort of mining are features, not bugs: they are what make Bitcoin secure. As long as miners have to spend real resources (electricity, hardware) to earn bitcoin, an attacker would have to spend extraordinary resources to override the honest consensus—and even then with no guarantee of success.

Bitcoin as a Protocol, bringing it all together

Through this clever dance of incentives and cryptography, Bitcoin achieves something groundbreaking: a decentralized consensus. Each miner is just trying to win some bitcoin by following the rules, but collectively their competition results in a ledger that everyone trusts as the truth, without needing any trusted arbiter. The double-spend problem—the risk that digital money could be copied or spent twice—is solved by the rule that the network only trusts the longest, Proof-of-Work-heavy chain, which one person can’t fake without outworking the world. “Proof-of-work has the nice property that it can be relayed through untrusted middlemen,” Satoshi wrote, meaning you don’t have to trust who gives you the data. You can verify the work itself. This mechanism directly addresses the institutional trust problem from Part 1. We no longer need a bank or clearinghouse to say “this transaction is good, that one is double-spent.” The Bitcoin protocol and mining network take care of it automatically.

With Proof-of-Work mining, Bitcoin provides a way for a global network to agree on a single ledger of transactions without trusting a central referee. This consensus protocol ensures that no fraudulent transaction or alteration can make it into the ledger unless an immense amount of work is done, far beyond what any attacker could likely muster. Combined with cryptographic ownership (private keys controlling funds), we now have a system where people can hold and transfer value online, directly, with trust placed in math and consensus rather than institutions. This solves the key issues of double-spending and the need for a trusted intermediary to validate transactions. We’ve essentially recreated the functions of a bank (keeping a ledger, verifying transactions, minting new currency) in a distributed, automated way. But one major aspect of “money” remains to to be examined. Bitcoin’s monetary policy: how new coins are issued, how the supply is controlled, and why this design choice matters. For that, let’s look at Bitcoin as an asset next.